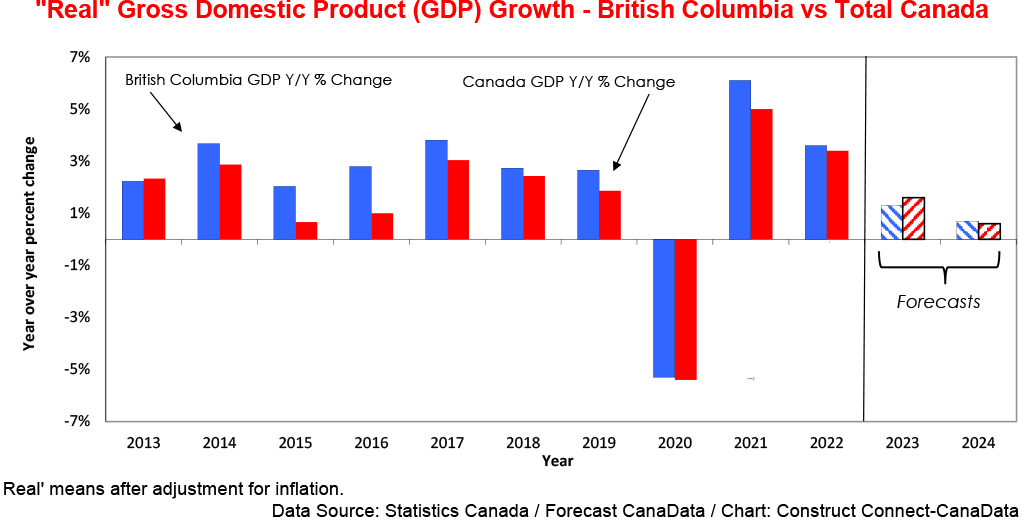

The recent ratification of a second (revised) agreement between the International Longshore and Warehouse Union and the B.C. Maritime Employers Association removes a big cloud of uncertainty that has hung over the B.C. economy since the beginning of July. Estimates of the time to clear the backlog and remove the kinks in the supply chain range from a few weeks to a couple of months.

Unfortunately, the settlement of the strike does little to offset the impact of other concurrent factors which have depressed the province’s growth over the past year and a half. First, the Bank of Canada’s efforts to cool inflation by raising interest rates (i.e., plus 450 basis points over the past 16 months) have significantly depressed the two most interest-sensitive components of domestic demand, consumer spending and home sales.

Furthermore, given that B.C. households are the most indebted in the country, it is not surprising that the year-to-date growth of retail sales in the province has been just +1.4%, which is lowest in the country and well under the national average of +2.9%.

High interest rates and house prices depress housing demand

Higher mortgage rates have also severely depressed home sales. Year-to-date, they are down by -30%. Over the past two months (May and June), however, they have recovered some lost ground and are now up by +15% y/y due to the combination of a record surge in international immigration and a steady decline in the supply of homes for sale.

Driven by this recent pickup in home sales, house prices, as indicated by the benchmark, have risen by +8.6% year to date. The recent downgrade by the Canadian Real Estate Association (CREA), of its Resale Housing Market Forecast, in the wake of the Bank of Canada’s further tightening of monetary policy, has cast a pall over the near-term outlook for home sales.

Given this lackluster near-term outlook for housing demand, we expect housing starts to lose some of the momentum they picked up over the past few months. Looking further ahead, the outlook for housing demand and new residential construction brightens later in 2024, given the sustained growth of net migration and some easing of monetary policy.

Weak commodity prices hurt value of exports

Another factor weighing on B.C.’s near-term prospects is net exports. After rebounding strongly during the first five months of 2022, the value of net exports is down by -10.5% year-to-date in 2023, mainly due to a sharp drop in commodity prices. Exports of forestry products are -45%; energy products, -29%; and metals, -12%.

In addition, the impact of higher U.S. interest rates on housing demand south of the border has dampened purchases of B.C. lumber. Going forward, in the near term, the prospect of further tightening by the Federal Reserve overshadows the outlook for U.S. housing demand. As a result, sales of B.C. lumber into the U.S. are likely to remain depressed through the second half of this year and into next.

Capital spending cools after two strong years

Forward-looking indicators of capital spending in B.C. are flashing yellow. Statistics Canada’s comprehensive non-residential capital and repair expenditures survey (a.k.a., the Capex Survey), conducted in Q4/2022 extending into early 2023, projected that the nominal value of private and public sector non-residential construction would retreat by just over -6% this year after posting a gain of +16% in 2022. Last year’s result was augmented by the Kitimat LNG project. That work is now tapering off.

According to the Capex Survey, both private and public capital spending is projected to shrink this year: private by -5.7% and public by -6.4%. This rather downbeat outlook for B.C.’s capital spending in the near term is reinforced by the -29.8% year-to-date drop in non-residential building intentions, with industrial at – 24% and institutional, -59%, offsetting a +9% increase in commercial building plans.

Providing the federal government adopts a more supportive approach to energy-related investment, there are several major projects which could drive capex in 2024 and beyond. These include the , the project, and the project.

Bottom Line

The settlement of the dockworkers’ strike will provide both consumer and business confidence with a much-needed temporary boost. However, as noted above, the more deep-seated problems facing the province will overshadow its economic health well into next year.

John Clinkard has over 35 years’ experience as an economist in international, national and regional research and analysis with leading financial institutions and media outlets in Canada.

Recent Comments

comments for this post are closed