As my colleague, Michael Guckes, is wont to say, every economic cycle is different. The study of ‘the dismal science’ (as economics has sometimes been labeled) in school lecture halls pretends otherwise.

Students are taught that actions taken of a certain fiscal or monetary nature will surely lead to predictable specific consequences. Raising income taxes will lower consumer spending; higher interest rates will weaken housing demand; etc. It is the second of these we will concentrate on further along in this article.

Students are taught that actions taken of a certain fiscal or monetary nature will surely lead to predictable specific consequences. Raising income taxes will lower consumer spending; higher interest rates will weaken housing demand; etc. It is the second of these we will concentrate on further along in this article.

Most of these ‘truisms’ retain their power. But as we are finding out every day now, they’re also being bent and stretched and sometimes even turned inside out because never before has there been three years of worldwide pandemic, accompanied by massive government support spending and a zero interest rate regime that is being followed by intended corrective measures that may not be hitting the mark.

For example, take U.S. ‘real’ (i.e., inflation-adjusted) gross domestic product growth (GDP). Since the Spring of 2022, the federal funds rate has been lifted eleven times, from effectively nil, to where it is now in a range of 5.25% to 5.50%, a 22-year high. Surely the nation’s unemployment rate must be experiencing a crisis and national output to have slipped into a stall.

Well, no, not really.

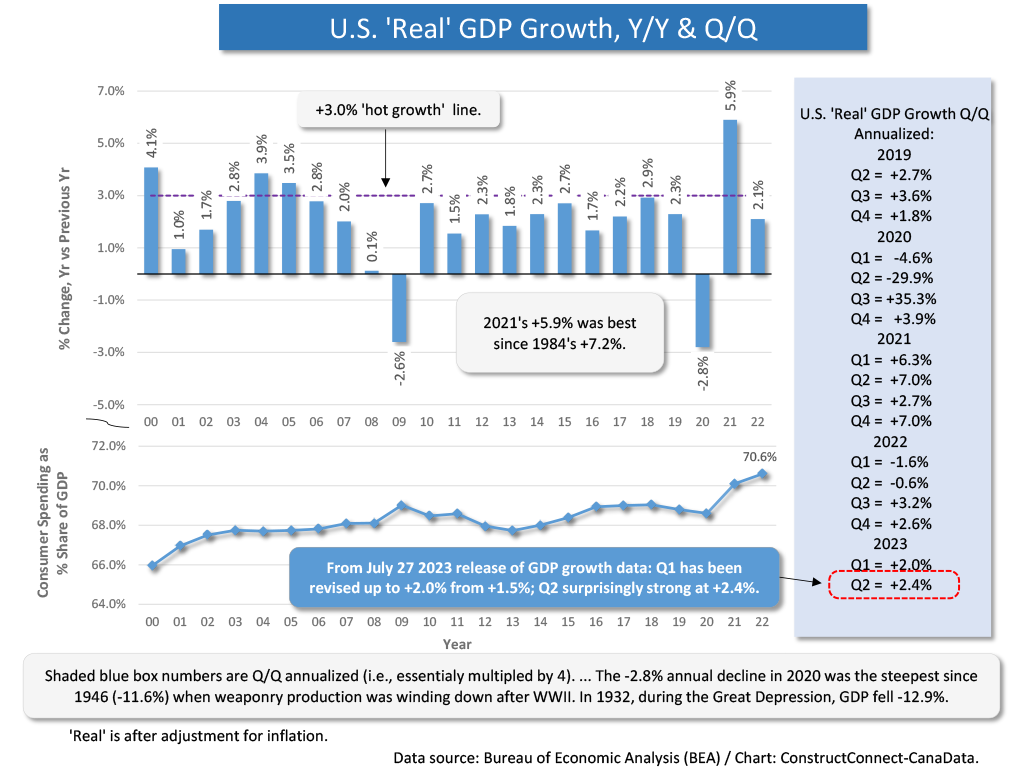

Second quarter U.S. GDP growth annualized, according to the latest data just released, was +2.4%, speeding up from this year’s first quarter figure of +2.0%. Over more than two decades, dating back to the year 2000, the average annual rate of U.S. GDP growth has been just over +2.0%; in other words, no different from now.

The current unemployment rate in America is 3.6% seasonally adjusted (SA), which is historically extremely low. The last time it was even as high as 4.0% was in January 2022. In other words, SA U has stayed under 4.0% for the entire duration of the Fed’s aggressive interest rate moves. That is not supposed to happen.

Inflation has come down significantly over the past year-plus, but maybe that is predominantly due to factors other than the rate hikes. The initial shock to the global food supply chain from the Russian invasion of Ukraine has dissipated to a fair degree and the ‘food at home’ line item within the U.S. Consumer Price Index (CPI) data set has eased back to +4.7% year over year, from double digit percentage increases earlier.

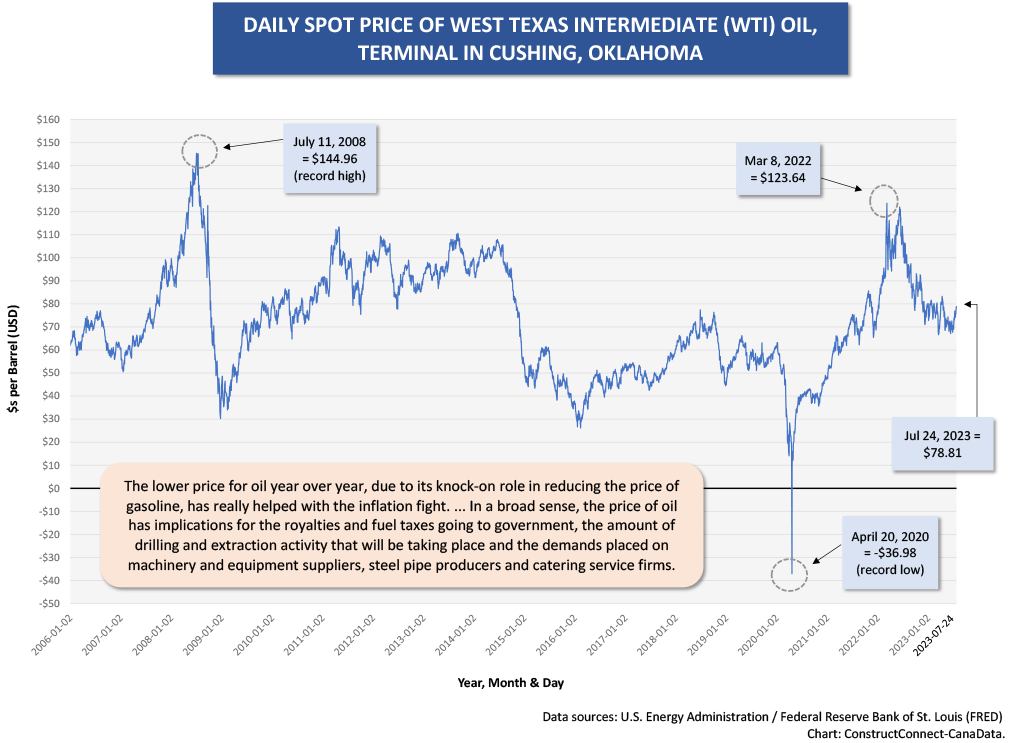

Most significant, the price of gasoline as a sub-index of the CPI is presently -26.5% y/y. The use of gasoline is so ubiquitous throughout almost all goods and service industries that when it is priced at a bargain, the knock-on benefits spread widely. The price of petrol domestically ultimately flows from the international market for crude oil, which can currently be characterized as tepid (Graph 2).

The overall inflation rate in the U.S. has now receded to +3.0% y/y. The inflation rate in Canada is even lower, at +2.8% y/y. The cost of gasoline north of the border is -21.6% year over year. The Bank of Canada’s key policy-setting interest rate, the ‘overnight’ rate, has been raised to 5.25%, a 22-year peak, the identical time span as in the U.S. Meanwhile, the R-3 unemployment rate, calculated on the same basis as in the U.S., is a mere 4.3%, not much above its all-time bottom.

(By the way, the component of Canada’s CPI termed ‘mortgage interest cost’ has shot up +30.1% y/y, in no way contributing to the fight against inflation.) ��

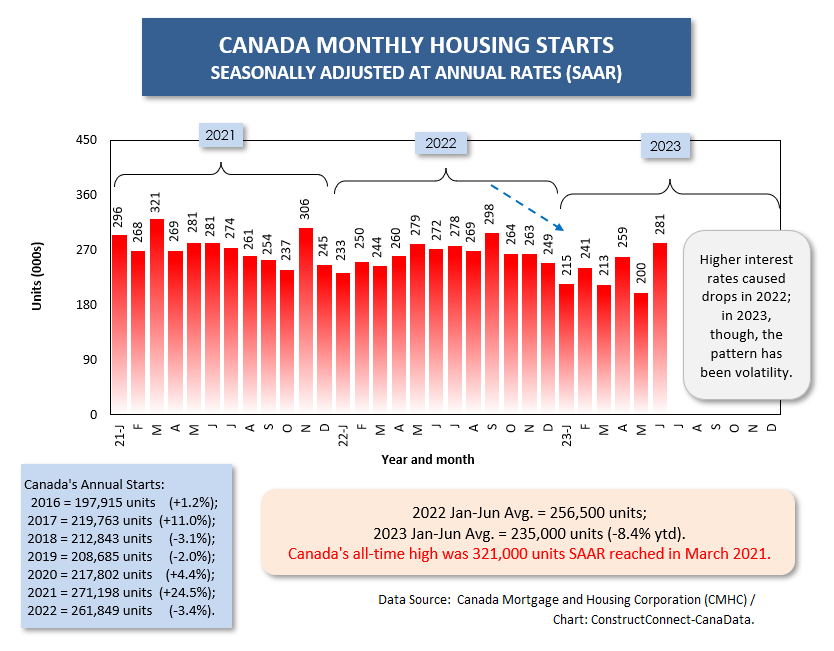

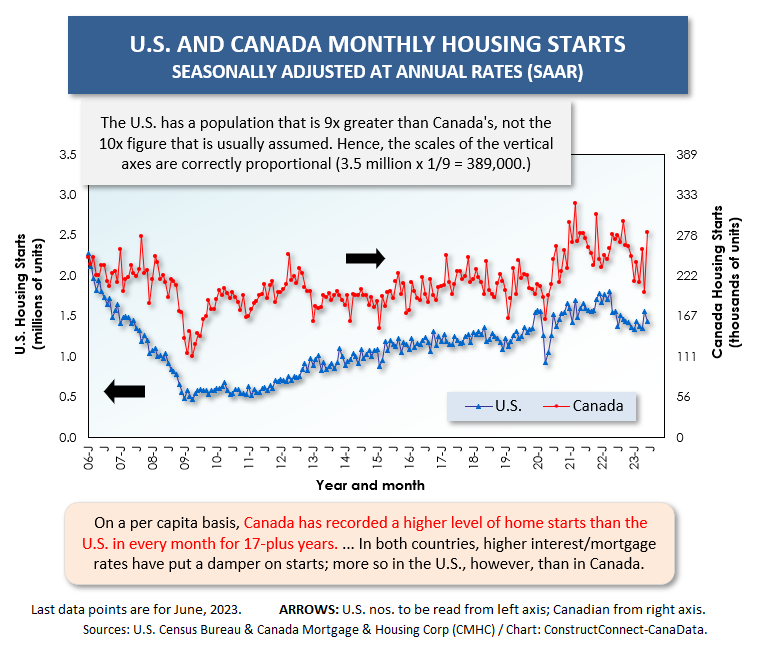

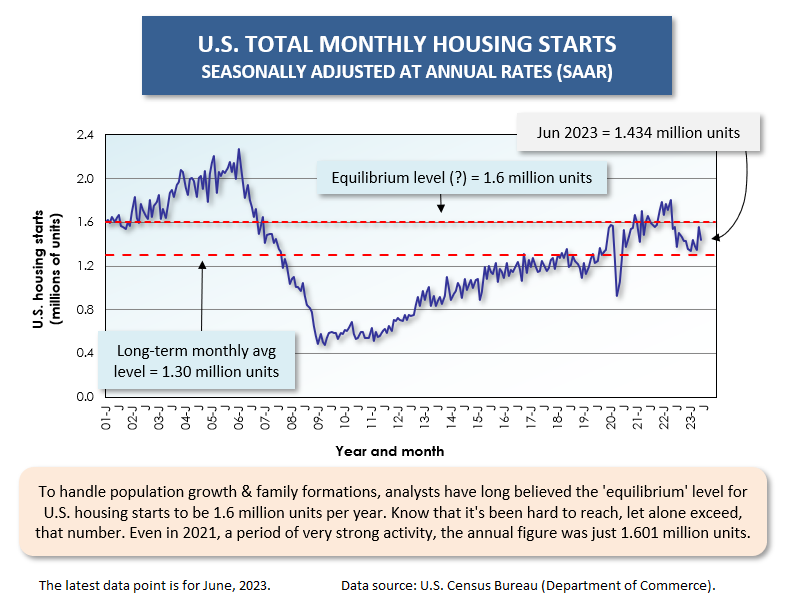

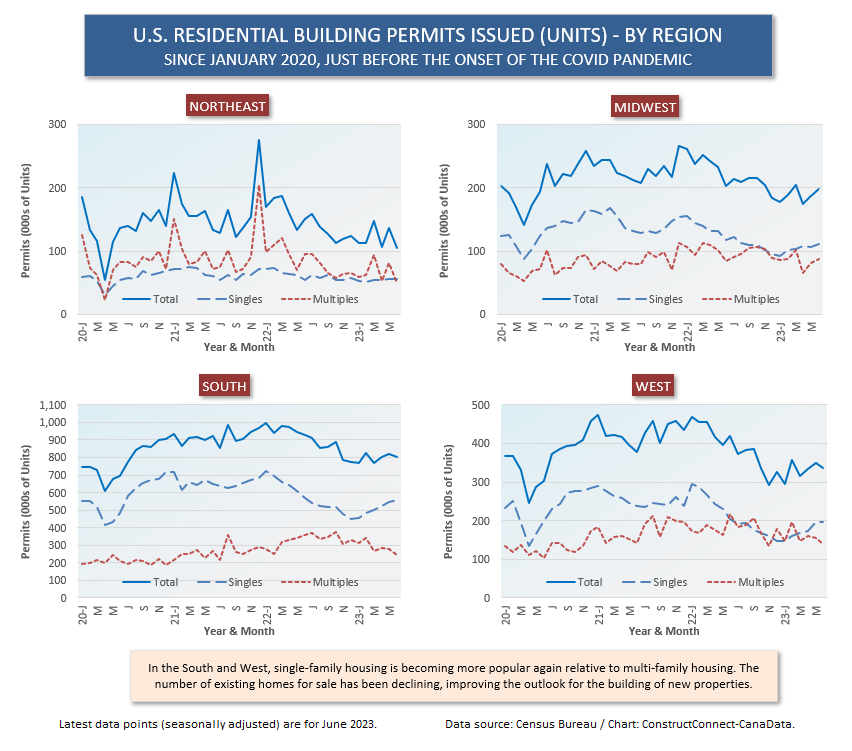

It is in the new homebuilding market, however, where footnotes will need to be added to economic orthodoxy in college textbooks. In both the U.S. and Canada, the early step-ups in interest rates did do harm to affordability and wreaked some havoc on ‘starts’ levels (see Graphs 3 and 4). In first half 2023, however, those effects have largely waned.

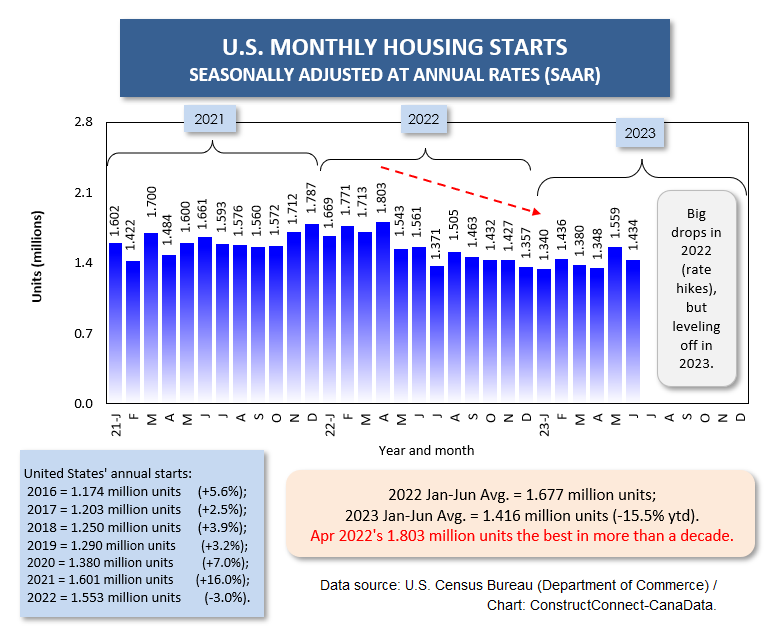

June’s figure on U.S. housing starts, at 1.434 million units, which was preceded by May at 1.559 million, nicely falls within the range that looks at the long-term average (1.3 million) and what is referred to as the ‘equilibrium’ level (1.6 million units; the annual number needed to accommodate population and family formation growth) (Graph 6).

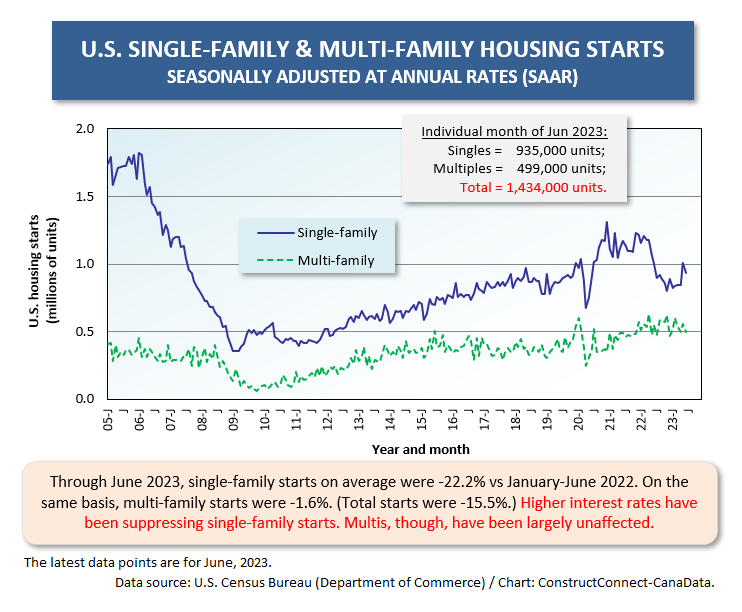

In the U.S., the most significant factor being credited for offering support to new home starts is the very thing designed to curb them, the elevated level of interest/mortgage rates. These are said to be locking people into their existing homes. Many homeowners are paying borrowing costs well below prevailing rates. The incentive to sell and ‘move up’, given what that would entail in terms of a higher carrying cost, has been taken away. The resulting supply shortage in resales is providing homebuilders with an opportunity.

Canada’s annual housing starts in the first two decades of this century averaged 200,000 units. In 2021, they jumped to 271,000 units. In 2022, under the negative influence of higher interest rates, they retreated a little to 262,000 units, with notable down-sliding in H2 of the year. But in 2023, the monthly annualized number has been quite volatile; in June, it rose to a stunning 281,000 units.

Canadian homebuilders understand that there is a long game to be played that will be driven by population growth. An immigration target of 500,000 individuals per year has been set for the foreseeable period ahead. Every two years, that’s the equivalent of an additional one-million person city. ��

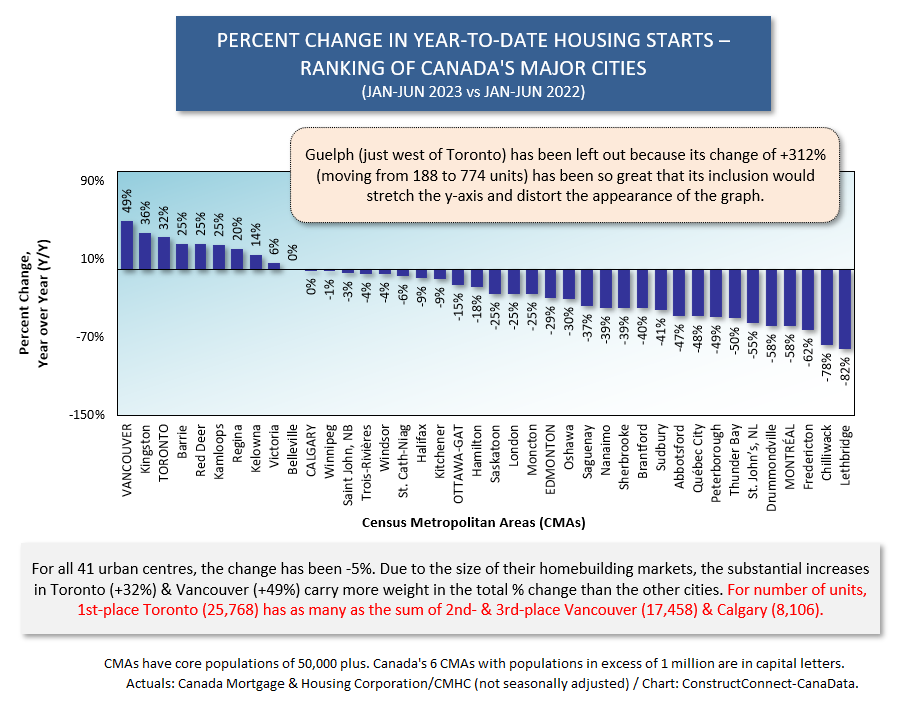

Perhaps the standout feature of Canadian housing starts so far this year has been how well Toronto has been doing. At 25,768 units (and +32% ytd/ytd), new home groundbreakings in TO have been as numerous as the next two cities in the ranking combined, Vancouver at 17,458 units and Calgary, 8,106 units.

But in case Torontonians feel they are entitled to swelled heads, they should consider their place in the joint U.S.-Canada new residential marketplace. South of the border, the two leading cities for new home foundation-laying, year-to-date, and measured according to building permits issued, have been Houston, 35,818 units, and Dallas-Ft Worth, 33,768 units.

Graph 1

Graph 2

Graph 3

Graph 4

Graph 5

Graph 6

Graph 7

Graph 8

Graph 9

Alex Carrick is Chief Economist for ����ӰԺ. He has delivered presentations throughout North America on the U.S., Canadian and world construction outlooks. Mr. Carrick has been with the company since 1985. Links to his numerous articles are featured on Twitter��, which has 50,000 followers.

Recent Comments

comments for this post are closed